Image

AFSA plays a vital role in supporting people experiencing vulnerability. Many people who access our services are already in financial distress and we want to ensure people who use our services receive the information that’s right for their situation.

After a period of consultation, we have launched our 3-year plan to ensure our service delivery supports clients experiencing vulnerability. This includes those facing compounding circumstances such as low literacy levels, mental health concerns and domestic violence.

Our vulnerability framework identifies, prioritises and supports people experiencing vulnerability in our system and sets out a plan to target our efforts over the next 3 years.

To learn more about the framework and our focus areas, visit our website.

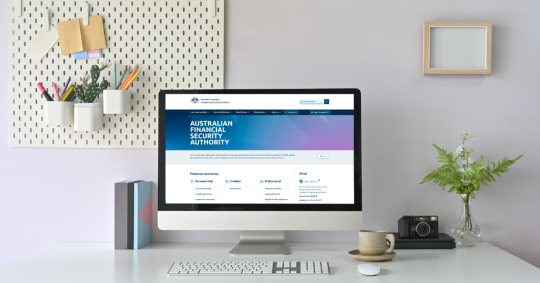

We’ve listened to your feedback and launched a new AFSA website to help our clients access our services and make informed financial decisions.

The new site features:

Explore the new site at afsa.gov.au.

We have released our Personal Insolvency Compliance Report 2021–22, providing a summary of how we supported at-risk users, drove willing compliance and engagement and addressed misuse in the insolvency system in the past financial year.

Between July 2021 and June 2022, we received 596 offence referrals, and served and issued 374 Official Receiver notices.

We also referred 126 briefs to the Commonwealth Director of Public Prosecutions (CDPP), and 95 individuals were prosecuted. 273 complaints were also investigated and resolved in the financial year.

Being visible, trusted and accessible is critical for effective regulation, and we strike a balance between firm and fair using strengths-based regulation. Key focuses in 2021-22 included:

To read our Personal Insolvency Compliance Report 2021–22, visit our website.

The media release is also available here.

Administrative news from Australian Financial Security Authority (AFSA).

AFSA is committed to enhancing our tools and services to improve user experience, reduce complexities and ultimately support positive regulatory outcomes.

We have recently made minor updates to the Bankruptcy Form to reduce the number of forms returned to debtors due to incompleteness or debts not provable in bankruptcy.

All forms should now be submitted using the new form which can be accessed through AFSA Online Services and the version number of the new form is 0922.

If you have any questions, please email registry@afsa.gov.au.

The Australian Financial Security Authority will be closed over the holiday period from close of business Friday 23 December 2022 and will reopen on Tuesday 3 January 2023.

More information is available on the AFSA website.

AFSA has published a range of case studies to showcase examples of exemplar behaviour from the insolvency sector. The case studies are real-life examples displaying best practice in culture, ethics and morality within the industry.

The latest case studies (5–9) are available on the AFSA website.

Recent floods have devastated many areas of Australia impacting thousands of people.

During this difficult period AFSA is committed to working as flexibly as possible with those who require our services who have been affected by the floods. This includes an ability to defer certain activities to ensure obligations of bankruptcy do not create an additional burden at what is already a challenging time.

Read more on our website.

The Australian Financial Security Authority (AFSA) recently made updates to our guidelines relating to the security of record storage for practitioners (Inspector-General Practice Guidance 2).

The updates include:

The purpose of this guidance is to outline our expectations about data and information management, and to provide practitioners with a set of principles to use in their decision making about the security and storage of information and administration records.

The public's focus on privacy and the security of their data and information held by organisations has increased, and it's extremely important that practitioners clearly understand their obligations and effectively manage cyber security risks. If you have any questions, please email practitionersupervision@afsa.gov.au.

AFSA has released its Annual Report 2021–22, discussing the agency’s operations and achievements in the last financial year. The full report is now available on the AFSA website.

AFSA Chief Executive Tim Beresford noted that there's an exciting future ahead for AFSA.

'The Annual Report acknowledges the successes of 2021–22, particularly those of our staff,' Mr Beresford said.

'In the face of large changes and ongoing challenges, our people have displayed resilience, professionalism and a generosity of spirit.'

'I'm looking forward to leading our team as we continue our commitment to be a firm and fair regulator and world-class government service provider.'

AFSA and the Inspector-General (IG) provide guidance across various subjects including:

This is consistent with our goal of delivering accessible, accurate and consistent information services, empowering clients and stakeholders to make informed decisions.

In our regulatory role, we cannot provide estate specific or individualised advice either verbally or in writing to practitioners on decisions made under bankruptcy legislation. We expect practitioners to exercise their own professional judgement to make decisions based on their knowledge and experience and, if necessary, advice from legal or other experts.

If you have comments or feedback about AFSA’s written guidance resources, please contact us at practitionersupervision@afsa.gov.au.

The latest practitioner news from the Australian Taxation Office (ATO).

A Trustee in Bankruptcy is required to meet certain taxation obligations under section 254 of the Income Tax Assessment Act 1936. If you have derived income, profit or capital gains in a representative capacity as a bankruptcy trustee during administering a bankrupt estate, you must apply for a TFN and lodge a tax return.

To apply for a TFN, you can either:

If you have not derived income, profit or capital gains in a representative capacity as a bankruptcy trustee, you do not apply for a separate TFN.

For further information refer to What bankruptcy trustees must do | ato.gov.au.

AFSA would like to note that we are presently finalising our guidance to practitioners on CGT and expect to publish this in the new year.

The Insolvency Industry Engagement team conducts Online services for business education sessions with insolvency practitioners.

During the education session, you can view real-time demonstrations of Online services functionality using your own systems. We can answer enquiries immediately and help your firm get the most out of the service. These sessions can be arranged at short notice.

More information

If you would like to find out more about using the ATO Online services for business, managing access or our education sessions, please email InsolvencyPractitionerServices@ato.gov.au.

For general information refer to the insolvency practitioners’ section on ato.gov.au/insolvency.

The enforceability of an Official Receiver notice to certain addressee types was recently revised.

In the event of non-compliance, where a company is the subject of an Official Receiver notice, it is sufficient to address the notice to the ‘proper officer’ as the correct addressee to ensure enforceable action.

Unless there is confirmation of who the proper officer is at a company, there is no requirement to have a person as an addressee on the notice.

Note: When a notice is issued to the ‘proper officer’, it is the responsibility of the company’s management to determine the appropriate person to action the notice. There is a chance that the person who responds to the summons may not have the correct information, and therefore it may be preferrable to address the notice by name to a director of the company.

The term ‘proper officer’ only applies to companies as they are a legal entity in their own right – the company itself is the defendant should a prosecution arise.

For any entity that is not a company, such as a business, firm, partnership, body corporate or sole trader, Official Receiver notices must be addressed to a natural person by name, i.e. Mr John Smith. The term ‘proper officer’ should not be used for these recipients. Proof of service must be obtained in case enforceable action is necessary.

NOTE: Case notes are necessarily incomplete. The only authoritative pronouncement of the Court's reasons and conclusions is that contained in the published reasons for judgment.

Issue

This matter concerns the proper construction and application of s 153(2)(b) of the Bankruptcy Act 1996 (Cth) (and the exception to discharge from bankruptcy in relation to a ‘debt incurred by means of fraud or a fraudulent breach’).

Section 153 relevantly provides that:

Background

In 2010 Mr Barodawala (the applicant) sued Ms Perinparajah (the respondent) in the New South Wales Supreme Court (NSW proceeding). He alleged that in 2008 she had engaged in misleading or deceptive conduct, amongst other things, in breach of the Trade Practices Act 1974 (Cth) (TPA). He made no express allegation of common law or equitable fraud in this NSW proceeding.

In 2011 Mr Barodawala, obtained a judgment under s 82 of the TPA against Ms Perinparajah, for being knowingly concerned in her company’s misleading or deceptive conduct. The Court entered judgment against Ms Perinparajah in the sum of $127,591.90. It also ordered Ms Perinparajah to pay Mr Barodawala’s costs. In March 2012, Mr Barodawala registered the NSW judgment in Victoria.[1]

Ms Perinparajah declared bankruptcy in April 2012 and, in November 2012, the trustee in bankruptcy admitted Mr Barodawala to vote in the amount of approximately $253,000 (reflecting the judgment debt and costs). Mr Barodawala received his petitioning creditor’s costs as a priority in the bankruptcy. However, it appears that he did not receive any amount referable to the judgment debt.[2]

On 18 May 2015, Ms Perinparajah was discharged from that bankruptcy.

Barodawala v Perinparajah [2021] VSC 387:

In March 2020, Mr Barodawala sought leave to enforce the NSW judgment against Ms Perinparajah by way of warrant of execution. Leave was granted in April 2020 and a warrant was issued in July 2020. In March 2021, Ms Perinparajah sought to set aside the warrant on the basis that she had been released from her provable debts by reason of her discharge from bankruptcy.[3]

Mr Barodawala submitted that Ms Perinparajah’s debt to him was incurred by means of fraud and thus section 153(2)(b) applied, such that Ms Perinparajah was not released from the debt. In July 2021 a judicial registrar rejected Mr Barodawala’s submissions and set aside the warrant.[4]

Barodawala v Perinparajah (No 2) [2022] VSC 247:

Mr Barodawala appealed from the decision of the judicial registrar to a judge in the Trial Division on the basis that Ms Perinparajah’s debt to him was incurred by means of fraud and thus s 153(2)(b) applied.

The primary judge dismissed that appeal, on the following two bases:

Analysis

As described above, Mr Barodawala sought leave to appeal from the primary judge’s decision on two proposed grounds:

Mr Barodawala accepted that he needed to succeed on both grounds in order to succeed in his proposed appeal.

Ground 1: As the phrase ‘debt incurred by means of fraud’ is used in s 153(2)(b) of the Bankruptcy Act, this appeal was to decide whether the judgement of debt falls within this scope. As a result, it questions whether Power v Kenny was wrongly decided.[7]

The primary judge held that there was no ‘debt incurred by means of fraud’ owed by Ms Perinparajah to Mr Barodawala upon Ms Perinparajah’s discharge from bankruptcy on 18 May 2015 because Mr Barodawala’s claim and cause of action had merged in the NSW judgment.[8]

Ground 2: The Court considered Ground 2 first and concluded, at paragraph 41:

that the NSW Reasons, upon which Mr Barodawala’s claim turns, do not support a conclusion that the debt owed by Ms Perinparajah to Mr Barodawala was ‘incurred by means of fraud’. That conclusion does not turn on any one single factor (such as the failure to expressly plead fraud, Ms Perinparajah’s failure to appear at the hearing of the NSW proceeding, or Ball J’s failure to make an express finding of fraud). Rather, it turns on the particular combination of factors present in this particular case.

Ground 2 was rejected by the Court, and Mr Barodawala’s proposed appeal couldn’t succeed. However, it was deemed appropriate for the Court to express their opinion on ground 1 in light of the importance of the issue and the fact that the point was fully argued before them.

In his reasons in support of that conclusion, his Honour commenced with a discussion of Power v Kenny.

At paragraph 62 of the judgement, the case is described as:

Power v Kenny concerned an attempt by the plaintiffs to enforce a judgment more than 12 years old. The judgment had followed a finding of fraudulent misrepresentation in the sale of a business by the defendant to the plaintiffs. The defendant failed to pay the sum of $6,975 (being the judgment debt and costs) and, as a result of the plaintiffs’ petition, the defendant’s estate was sequestered. During the administration of the defendant’s bankrupt estate the plaintiffs received $4,787 in dividends. In 1972, the defendant was discharged from bankruptcy. The plaintiffs submitted that the defendant’s discharge from bankruptcy had not released him from his debt to them, by reason of s 153(2)(b) of the Bankruptcy Act.[9]

The primary judge observed that Wallace J held that the debt incurred by means of fraud had merged into the judgment, thus becoming res judicata and extinguishing the cause of action in fraud. After release from bankruptcy, there was no existing ‘debt incurred by means of fraud’ within the meaning of s 153(2)(b) of the Act.[10]

The Court, in this instance, had to consider whether the applicant’s original claim under the TPA constituted ‘a debt incurred by means of fraud’ and, if that was affirmed, whether that character ceased upon judgment being entered in 2011 due to doctrines of merger by judgment and res judicata.

In its contemplation of the legislative provision, the Court in this proceeding noted, at paragraph 59, that:

the starting point in any exercise of statutory construction is the text of the provision. However, the text is to be considered in light of its context and purpose. Context includes the legislative context, because the meaning of a provision must be determined by reference to the entire Act.

Thorough consideration was given by the Court as to the context and purpose of the Bankruptcy Act 1996 (Cth) s153(2)(b) specifically, the Act generally and the consequences of competing interpretations, as well as consideration of comparative authorities from United Kingdom and Canada.

At paragraph 79, the Court accepts Mr Barodawala’s submission that, if Parliament had intended to exclude judgment debts from the operation of s 153(2)(b), it would have done so expressly.

At paragraph 113, the Court determines that “the approach adopted in Power v Kenny and by the primary judge does not advance the purpose of the Act and produces illogical consequences”.

The Court decided that doctrines of merger by judgment and res judicata did not mean a debt was not ’incurred by means of fraud’ and that there was no implied restriction in operation of s 153(2)(b), based on principles relating to finality in litigation.

Decision

In concluding, Sifris JA concluded that Mr Barodawala made good his case in relation to ground 1 and the Court determined, at paragraph 114, that:

a judgment debt will be a “debt that was incurred by means of fraud” within the meaning of section 153(2)(b) if the original debt on which the creditor sued was incurred by reason of the fraudulent conduct of the debtor.

Following that, the Court determined that Power v Kenny was wrongly decided.

However, as the Court rejected ground 2, the Court granted leave to appeal but dismissed the appeal.[11]

Footnotes:

[1] At paragraph 3

[2] At paragraph 4

[3] At paragraph 6

[4] Ibid

[5] [1977] WAR 87

[6] Barodawala v Perinparajah (No 2) [2022] VSC 247, [81] (‘Reasons’).

[7] At paragraph 43

[8] Barodawala v Perinparajah (No 2) [2022] VSC 247, [81] (‘Reasons’)

[9] Power v Kenny [1977] WAR 87, 88.

[10] Barodawala v Perinparajah (No 2) [2022] VSC 247, [23] (‘Reasons’)

[11] At paragraph 115