Image

If a secured creditor realises its security while the agreement is in force, the (formerly secured) creditor is taken to be a creditor only to the extent of any outstanding provable debt. Any interest accrued on the debt after acceptance of the debt agreement proposal for processing cannot be recovered via the debt agreement.

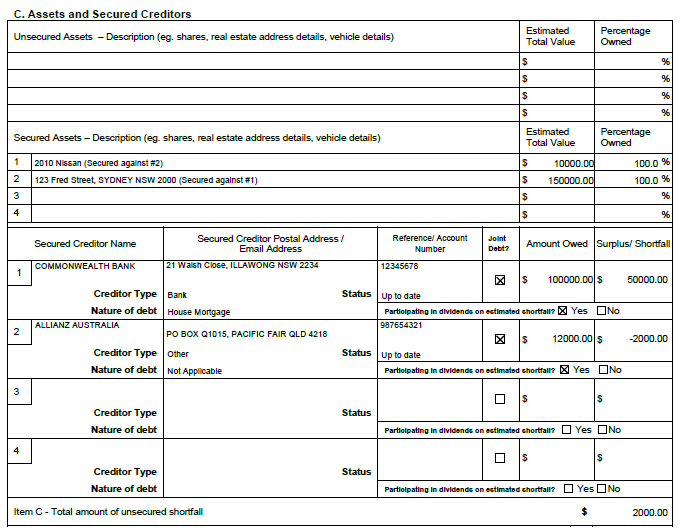

A debtor is required to disclose all of their liabilities on the debt agreement explanatory statement, irrespective of the particular categories into which the debts fall.

The total unsecured debts include any shortfall between a secured debt and the value of the security.

The term undue hardship is defined in section 111 of the Bankruptcy Regulations, which relates to requests to the Inspector-General for waiver or remission of charges, as follows:

A secured creditor is entitled to vote for the shortfall after deducting the value of security or for any actual shortfall after repossession and sale.

Subsection 185C(2) of the Bankruptcy Act also provides that creditors are not entitled to receive more than the amount of their provable debt. This may require amendments to the value of securities. Administrators must ensure that, where secured creditors are still receiving payments from the debtor, payments are not made to secured creditors with respect to the unsecured portion of their claims if the claims of the secured creditor have been satisfied in full.

The Official Receiver may reject a proposal to vary a debt agreement if the Official Receiver reasonably believes that the agreement as proposed to be varied would cause undue hardship to the debtor. This is applicable only to proposals to vary agreements where the original debt agreement proposal was given to the Official Receiver on or after 27 June 2019. For considerations regarding the Official Receiver’s power to reject a proposal to vary for this reason, see above.

| Completion of the debt agreement/discharge of all the debtor’s obligations under the debt agreement (as per section 185N of the Bankruptcy Act) |

The NPII record will be removed in one month of the following:

whichever is later |

|

Termination of the debt agreement, where the termination:

|

The NPII record will be removed in one month of the following:

whichever is later |

| Where an order of the Court declared the debt agreement void (in accordance with section 185U of the Bankruptcy Act) |

The NPII record will be removed in one month of the following:

whichever is later |

|

Where a debt agreement proposal was lodged and it:

|

The NPII record will be removed within one year of the relevant event |

| Situation | The retention period for the information is whichever of the following periods ends later |

|---|---|

| a debt agreement that ends under section 185N of the Bankruptcy Act (s185N of the Bankruptcy Act relates to the completion of a debt agreement by making all payments) |

|

| a debt agreement that does not end by all payments having been made |

|

|

a debt agreement proposal that:

|

the day that the:

|